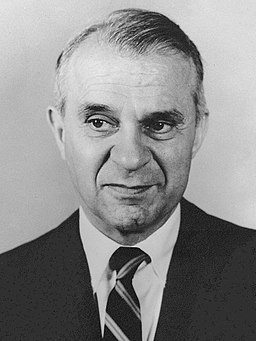

Abba Lerner was the milton friedman of the left. Like Friedman, Lerner was a brilliant expositor of economics who was able to make complex concepts crystal clear. Lerner was also an unusual kind of socialist: he hated government power over people’s lives. Like Friedman, he praised private enterprise on the ground that “alternatives to government employment are a safeguard of the freedom of the individual.” Also like Friedman, Lerner loved Free Markets. He opposed Minimum Wage laws and other price controls because they interfered with the price system, which he called “one of the most valuable instruments of modern society.”1

Both his clear writing and his hatred of authority are illustrated in the following defense of consumer sovereignty:

One of the deepest scars of my early youth was etched when my teacher told me, “You do not want that,” after I had told her that I did. I would not have been so upset if she had said that I could not have it, whatever it was, or that it was very wicked of me to want it. What rankled was the denial of my personality—a kind of rape of my integrity. I confess I still find a similar rising of my hackles when I hear people’s preferences dismissed as not genuine, because influenced by advertising, and somebody else telling them what they “really want.”2

Lerner, like Friedman, had a sharp analytical mind that made him follow an argument to its logical conclusion. During World War II, for example, when john maynard keynes gave a talk at the Federal Reserve Board in Washington, Lerner, who was in the audience, found Keynes’s view of how the economy worked completely convincing and challenged Keynes for not carrying his own argument to its logical conclusion. Keynes denounced Lerner on the spot, but Keynes’s colleague Evsey Domar, seated beside Lerner, whispered, “He ought to read The General Theory.” A month later, wrote Lerner, Keynes withdrew his denunciation.

Lerner was born in Romania and immigrated with his parents to Britain while still a child. He tried out several avocations: as tailor, Hebrew teacher, typesetter, and owner of a printing business that went bankrupt during the Great Depression. He turned to economics, enrolling in a night course at the London School of Economics in 1929, in order to discover why his business had failed. Lerner earned top honors and several scholarships for his logically reasoned essays, many of which were published while he was still an undergraduate. His appointment as assistant lecturer at the LSE in 1936 was the first of many teaching positions, the rest of which he held in the United States after 1937. paul samuelson, in a tribute to Lerner on his sixtieth birthday, wrote that Lerner’s experience “tempts one to advise students in Economics A to quit college, fail in business, marry and raise a family, and resist being overpaid.”3

One of Lerner’s first papers, published in 1934, is a clear diagrammatic exposition of international trade. Earlier, he had written, but not published, a proof of the conditions under which free trade in goods causes the prices of factors to be equal even when factors are immobile. Samuelson showed the same thing in an article much later. “After I had enunciated the same result in 1948,” Samuelson later wrote, “Lord Robbins mentioned to me that he thought he had a seminar paper in his files by Lerner of a similar type…. He exhumed this gem, which appeared 17 years later in the 1950 Economica.”4

Probably Lerner’s best-known article is “The Concept of Monopoly and the Measurement of Monopoly Power.” In it he laid out clearly why setting the price of a good equal to its marginal cost is important for efficiency. The amount by which the price exceeds marginal cost is a measure of monopoly power in an industry. In 1964 Samuelson wrote: “Today this may seem simple, but I can testify that no one at Chicago or Harvard could tell me in 1935 exactly why P = MC was a good thing.”5

Lerner’s main contribution to macroeconomic policy is his concept of functional finance. Lerner thought that if governments wanted to increase aggregate demand so as to maintain employment, and if the federal budget was balanced, the government should run a deficit by increasing government spending or decreasing taxes. If, on the other hand, the government wanted to decrease aggregate demand, it should, if the budget was balanced, run a surplus by decreasing government spending or raising taxes. These thoughts are often attributed to Keynes, and they do follow from Keynes’s reasoning. But Keynes never stated them. It took Lerner’s clear thinking to get from Keynes’s model of the economy to these policy conclusions. Lerner’s thoughts are attributed to Keynes because textbook writers, wanting to make Keynes’s thinking clear, were immediately drawn to Lerner’s thinking. As economist David Colander has written, Keynes could be considered just as much a Lernerian as a Keynesian.

Lerner was active in economic analysis until the day he died. In 1980, for example, he laid out a plan for breaking OPEC. In an article titled “OPEC—a Plan—If You Can’t Beat Them, Join Them,” Lerner advocated that the United States and other governments of oil-consuming countries impose a 100 percent excise tax on the difference between OPEC’s price and the pre-OPEC price adjusted for inflation. In 1980 OPEC charged twenty-six dollars for a barrel of oil. The pre-OPEC price adjusted for inflation was six dollars. Therefore, at that price, the tax would have been 100 percent of 26 − 6, or twenty dollars. Lerner’s plan, if followed, would have caused the price to consumers to rise two dollars every time OPEC raised its price one dollar. More important, it would have caused the price to fall by two dollars every time OPEC lowered its price by one dollar. Lerner’s thinking, which was absolutely watertight, was that this plan would double consumers’ elasticity of demand, causing them to demand less oil at higher prices and thus reduce the strength of the cartel. The plan was never adopted.

Lerner never developed a following. One reason, wrote Tibor Scitovsky of Stanford, was “Lerner’s unrelenting logic,” which “overruled whatever loyalties he started with” and “made him seem like a cold fish to just about everybody.”6 Another reason was that Lerner rarely stayed in one university long; he taught at Columbia, the University of Virginia, Kansas City, Amherst, the New School for Social Research, Roosevelt, Johns Hopkins, Michigan State, and the University of California at Berkeley. Another reason was that although he made major contributions in so many areas, he did not have a specialty. Also, Lerner made his insights so clear and so apparently obvious that people who adopted his ideas forgot where they learned them. Probably because he lacked a following, Lerner never received the Nobel Prize, although many economists think he should have.

Selected Works

1934. “The Concept of Monopoly and the Measurement of Monopoly Power.” Review of Economic Studies 1: 157–175.

1934. “The Diagrammatical Representation of Demand Conditions in International Trade.” Economica, n.s., 1 (August): 319–334.

1936. “The Symmetry Between Import and Export Taxes.” Economica, n.s., 3 (August): 306–313.

1943. “Functional Finance and the Federal Debt.” Social Research 10: 38–51.

1944. The Economics of Control: Principles of Welfare Economics. New York: Macmillan.

1972. “The Economics and Politics of Consumer Sovereignty.” American Economic Review 62 (May): 258–266.

1980. “OPEC—a Plan—If You Can’t Beat Them, Join Them.” Atlantic Economic Journal 8, no. 3: 1–3.

Footnotes

1.

Tibor Scitovsky, “Lerner’s Contributions to Economics,” Journal of Economic Literature 22, no. 4 (1984): 1549.

2.

From “The Economics and Politics of Consumer Sovereignty,” p. 258.

3.

Paul A. Samuelson, “A. P. Lerner at Sixty,” Review of Economic Studies 31, no. 3 (1964): 169.

4.

Ibid., p. 172.

5.

Ibid., p. 173.

6.

Scitovsky 1984, p. 1549.

(0 COMMENTS)